Why I'm Short Lightspeed Commerce Inc. $LSPD.TO

The Bubble that is bound to burst.

Introduction

Lightspeed commerce provides a commerce software platform (SaaS) for small and mid-size businesses in Canada, Germany, United States and internationally. The software as a service (SaaS) platform allows business owners to accept payments, manage operations and engage with customers. In addition, Lightspeed also sells point of sales technology for accepting payments in brick and motor stores. Sound familiar? Probably because you’ve might’ve heard of either Shopify, PayPal and/or Square. Not only do I think the majority of the sector is egregiously overpriced, but I think that Lightspeed is the dirtiest shirt in the hamper with their share price completely diverging from their underlying value.

Lightspeed: Unimpressive Go-to-Market Strategy.

Lightspeed generates revenue through subscription fees, transaction fees and hardware sales, similar to both Square and Shopify. Lightspeed’s platform although doesn’t really differentiate itself from neither Square or Shopify, the management seems to believe that charging more and providing less is a good long-term strategy.

I will not go into heavy detail on each individual package, I will just compare the Lightspeed Lean package versus the Basic Shopify package. The features for the Shopify Basic package are that they allow you to sell unlimited products, provides a custom store builder, marketing tools, shipping options and can connect up to four physical store locations. LightSpeed’s Lean package, gets you a retail POS system with 1 register and integrated payments. In addition, Shopify is integrated with over 4,100 different applications across diverse categories such as accounting, customer service, branding and pop-ups, whereas Lightspeed only has 45 app integrations. Not only does the initial Shopify package provide more and charge merchants less, but the software also integrates with significantly more tools than the Lightspeed Lean package. Furthermore, other competitor Square, charges merchants no monthly fee for e-commerce and only charges them a commission per transaction. Keep in mind, Shopify and Square both have much greater portions of the market and both have significant brand recognition. For Lightspeed to offer less value and charge customers on the high side, provides me with doubt that their recent top line success will continue to persist even in a fast growing sector.

Expensive Customer Acquisition Cost and Choppy Bottom Line.

In 2020 Lightspeed saw its merchants increase from 49,000 to around 76,500 which at first glance is impressive, however their largest domestic competitor Shopify saw their merchants increase by 749,000 in 2020. In addition, it cost Lightspeed $3,529.00 to acquire 1 new customer during that year whereas Shopify only paid $803.00 to acquire 1 new customer. The two main reasons as to why I think Lightspeed’s CAC are so high is because firstly, they’re expensive for merchants to use and secondly they face stiff global competition. The problems however don’t stop at just customer acquisition, Lightspeed’s entire bottom line remains choppy as EBIT margins continue to decline despite the pandemic and huge merchant growth.

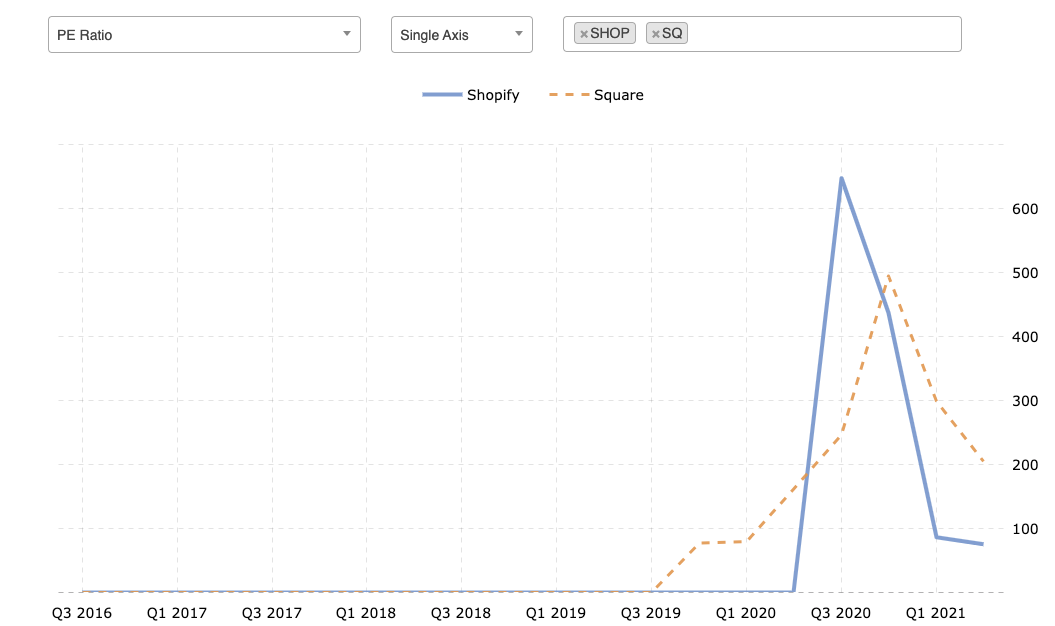

Valuation: Sector is Valued Ugly but Lightspeed is Valued Uglier.

When looking at the SaaS sector in relative to the general market, you realize how overvalued the entire sector is. The PE ratio for the SaaS sector is 82.96 compared to the S&P 500’s 46.19 which is almost half. If we look even deeper, Lightspeed’s two largest direct competitors Square and Shopify are immensely overvalued as well.

Lightspeed however is priced even worse than both Square and Shopify in my opinion, the company is currently at a 13 billion dollar market cap (USD) with only 300 million (USD) in revenue YTD. In addition, the firm has never turned a profit and bleeds cash. Lastly, Lightspeed may have shown impressive sales growth in 2020 and now 2021, but I’m not entirely sure how much of that was attributed to Covid-19.

Final Thoughts

It is one thing to price in the growth of a company, but it becomes another thing when you begin to price in insanity. Lightspeed is currently trading 45 times its sales and has a go-to-market strategy in which I think will diminish EBIT margins and sedate long-term growth. Also, predicting Lightspeeds future growth will be extremely difficult as there is stiff global competition. Therefor, I think to price as much growth as the market has into Lightspeed is dangerous and investors should stay away. Lightspeed is currently priced at $96.51 on the NYSE and at $122.18 on the TSX and my price target is $20 USD.