Gran Tierra Energy Remains Undervalued.

Why I love Gran Tierra Energy and why it remains my favourite oil play.

Introduction

Gran Tierra Energy ($GTE) is an oil and gas exploration and production company with operations in Colombia and Ecuador, headquartered in Calgary Alberta. All of Gran Tierra’s revenue comes for their drilling assets located in the Middle Magdalena Valley in Colombia with the Acordionero Field being their largest producer of oil with roughly 49% of their current production. Gran Tierra’s stock has become completely distraught over the past couple of years due to low oil prices, increasing debt loads and sub-par management decisions. Gran Tierra’s problems were magnified when the Covid-19 shock hit the oil market and the firm was and has remained priced for bankruptcy ever since. I am of the opinion that we have seen the worst of Gran Tierra’s hurtles and blows to the share price and we will see an intense rebound from them over the next 2-3 years. I am going to divide this article into the 3 major concerns investors have of Gran Tierra Energy, oil prices, debt load and political unrest in Colombia and attempt to explain why each of these concerns are widely oversold. Lastly, I will give you my overall price target for the company and my reasoning for it.

Oil Prices: The Rally is Secular

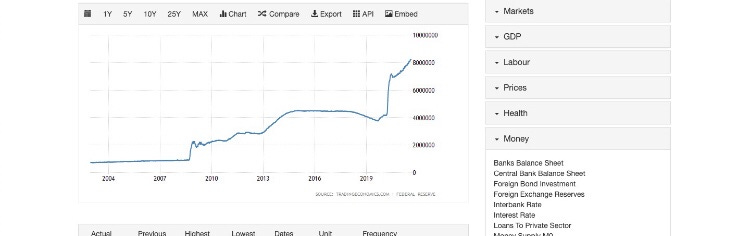

The first concern I must address is the wide spread opinion that the recent oil rally we’ve seen over the past couple of months is “transitory”. I believe crude oil prices will not only remain this high, but even have potential to move up higher as ESG investing and progressive governments attempt to rein in on the production of oil. The oil sector has become fully aware that they do not have the same cushion financing they’ve once had due to financial intermediaries actively pursuing green investments in replacement of fracking and drilling. For this reason, I expect CapEx to remain relatively low in the sector keeping the supply side tight. In addition, I think the currency in which oil is priced in the U.S Dollar, has potential to decline in the future due to large trade deficits and quantitative easing. In 2020, the U.S M2 monetary aggregate increased by 25% and the Federal Reserve’s balance sheet has now totalled 7 trillion dollars with the FOMC still denying the possibility of secular inflation. Due to the Feds reluctancy to shrink the balance sheet and to remove the market punchbowl, the DXY (U.S Dollar Index) has the possibility of hitting 85 or even lower.

U.S Central Bank Balance sheet year-to-date. Source: Trading Economics.

Now lets say oil does not move up and consolidates from around $65-75, this still remains a fantastic price area for Gran Tierra to increase cashflow and deleverage.

High Debt Load: Why it Doesn’t Matter

The second problem investors have with Gran Tierra is their debt load. Gran Tierra Energy currently has a long-term debt load of 759 million dollars which is around 3.6 times its current market capitalization. Now at first glance this sounds awful, however the debt is well laddered providing management breathing room to pay it down. The debt is currently broken down into 3 portions, a 175 million dollar revolving credit facility, 300 million in senior notes due in 2025 and 300 million in senior notes due in 2027. The firm has already taken initiative by paying down 15 million of its revolving credit facility over the first two quarters of 2021 and they intend on reducing the balance down to around 70 million by the end of year. I believe as long as Brent trades above $70 and production remains at 30,000-32,000 BOPD in the second half of the year, Gran Tierra will be successful in reducing the revolving portion down to $70-80 million by the end of 2021. Also, as I said before I believe the oil rally is secular, giving Gran Tierra a high margin of error before a bankruptcy were to eventuate.

Colombia’s Political Unrest

Lastly, Colombia is currently under severe political tension after protest began in April when President Duque proposed controversial tax reforms which caused an outcry on the citizens of Colombia. These protest became extremely violent and caused blockades all over the country causing Gran Tierra to temporarily shut down some of its production. I do not expect these protest to go away anytime soon as it seems like the protest are more than just about tax reform, but rather a demand for changes on the underlying fundamentals on which the country is governed. That being said, the riots have reportedly calmed down and President Duque has since withdrawn the tax reform and is looking to propose a new one that better suits the Colombian citizen’s demands. In addition, Gran Tierra had announced a few weeks back that it had recently restored the production which was halted as a result of the protest which indicates a good sign of tensions easing near their operations.

The Bull Case for $GTE

Gran Tierra has one competitive advantage over a lot of drillers and it is simply its size and geography. Gran Tierra’s operations being located in Colombia may have its disadvantages, but it also has its perks. Colombia is a warmer climate country which usually equates to better margins per barrel of oil than in a colder country such as Canada. Furthermore, Colombia provides investment incentives such as tax credits to its oil industry where developed nations like Canada and the United States are pressuring large oil firms to comply with new sorts of environmental policy. Over the past few months big names such as Shell, Suncor and Exxon Mobile have all been facing headwinds due to political pressure and in the case of Exxon, climate change proxy fights. Gran Tierra does not need to worry about any of these at the moment because of their size and the location in which they operate in. This reduces a risk factor that the large oil firms may have to endure in future years. Lastly, with all the risks associated with Gran Tierra Energy, they are all extremely mitigated if oil remains above $60 per barrel. For these reasons, Gran Tierra should currently not be priced as if they are about to go bankrupt and GTE currently presents a deep value opportunity.

Conclusion

I believe Gran Tierra Energy has seen the last of its headwinds and will begin to make progress in cleaning up the mess that lockdowns and nationwide protest have caused to its share price. I believe that as long as oil remains at these price levels, the margin of error for the company remains extremely high and that the financial health of the firm is no longer in jeopardy. For the reasons listed above, I believe that Gran Tierra Energy is currently trading well below its intrinsic value and show a great amount of upside. Gran Tierra is currently trading at $0.71 per share and my consensus estimate over the next 2-3 years is for it to hit $3.50 per share. Please keep in mind that I am not recommending this play to anyone and it is merely just my opinion.