Camping World Holdings $CWH: Why I Think this Stock could Double.

| Seeking Alpha")

Introduction

Camping World Holdings is a recreational vehicle (RV) and outdoor retailer in America. The firm operates through two main business segments, Good Sam Services and Plans and Outdoor Retail. The company has seemed to have had a recent uptick in 2020 and now 2021 with sales and net income growing at an increasingly rapid pace. I attribute this uptick to Covid-19 flight restrictions and lockdowns changing consumer travel behaviour. I also believe Camping World’s management has done an amazing job of expanding their higher margin business segments and creating a strong outdoor recreation network. Despite Camping World’s astounding performance over the past year and management increasing the firms share repurchases and dividend payouts, Camping World is still priced at just 7 times earnings and has a short % of float of 18%. I am of the opinion, that the market simply has this company priced completely wrong, and I am going to explain why in this article.

Attractive Valuation: A Growth Stock that is Priced at Deep Value.

Camping World Holdings is currently egregiously undervalued when you take into account its valuation metrics in comparison to competition.

Using a Comparable Cost Analysis, you see that Camping World is priced way below the industry median in every metric across the Recreational Vehicle industry. In addition to doing a CCA analysis, I also conducted a Discount Cashflow Model using an 8% growth rate, 12% discount rate, 3% perpetuity rate and 522 million year-to-date FCF.

My consensus from doing the DCF model is that Camping World’s shares are currently trading at a 41% discount. Based on my CCA and DCF model’s Camping World is trading at a bargain, but in order for me to have a coherent consensus on the security I must also analyze the firms qualitative characteristics.

Higher Margin Business Segments and New Forms of Value Creation.

Camping World has done a very good job over the past few years transitioning itself from just being an outdoor/RV retailer to creating an ecosystem in which encompasses Insurance offerings, vehicle financing, memberships, trip advice, roadside assistance services and RV appraising. I find these new business segments are not only more lucrative, but help increase customer acquisition and retention. Camping World is slowly becoming a one stop shop for all your outdoor/RV needs from helping camping novices to experts. Below is Camping Worlds Q2 revenue by segment.

Although new and used RV sales make up approximately 74% of Camping World’s Q2 2021 revenue, the gross margins in their other segments gives them incredible potential to create increasing value for shareholders.

If Camping World’s higher margin segments continue to build momentum, the firm will be able to grow its net income seamlessly and set themselves apart from its competition.

RV Industry: Positive Economic Outlook.

Recreational Vehicles and Outdoor Camping has become increasingly popular over the Covid-19 pandemic due to flights being cancelled and peoples desire to find a way to travel. That is why according to ITR Economics, RV shipments are expected to increase by 20% in North America by the end of 2021. Since flight restrictions and cancellations seem to be inevitable for an indefinite period of time, there could be a massive change in consumer behaviour when it comes to travelling. This puts Camping World in a fantastic position to acquire new customers and build value because all of Camping World’s highest margin products/services add value to the new comer to outdoor recreation/camping.

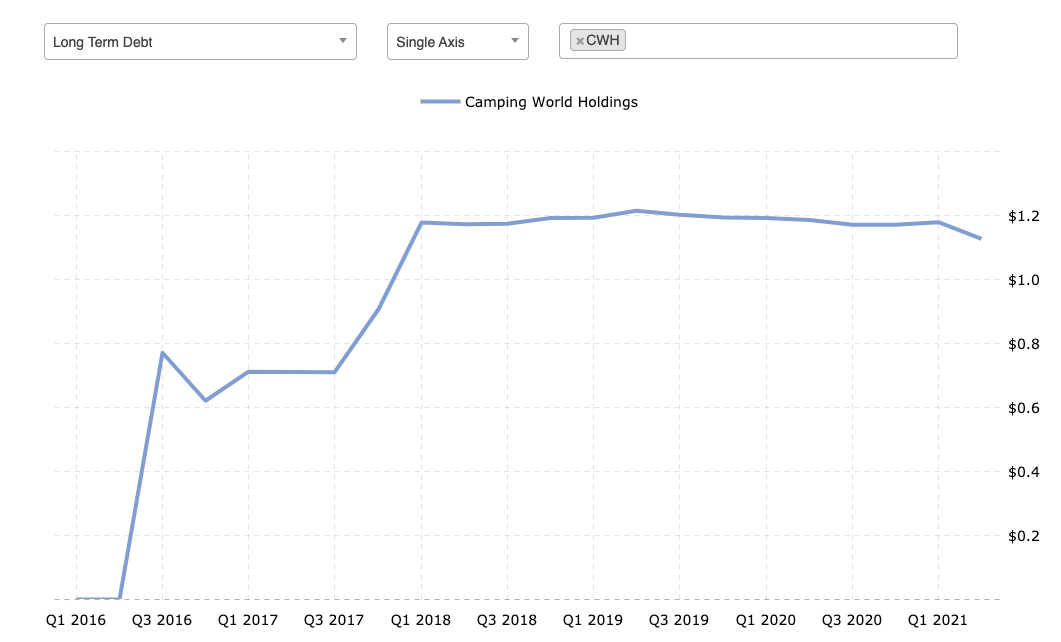

A Quick Word on Debt

Lastly, I would like to mention Camping Worlds Debt. Camping World Holdings currently has a higher than average debt-to-equity and debt/ebitda ratio than their industry median. The firm currently sits on 1.13 billion dollars of long-term debt.

My quick take is that the debt is well laddered with the majority portions not due until 2026 and 2028 and Camping World projects to earn more than enough cash to deleverage itself over the near to mid future. In conclusion, the firms 52 week return on invested capital (ROIC) is 46%, meaning the firm has been allocating their capital well.

Conclusion

Camping World Holdings remains one of my top picks for the years 2021 through 2023. I believe that their value proposition to new comers in the RV space is going to allow them to expand their business far more than the competitions. Furthermore, CWH continues to differentiate itself in an industry that I think is going to grow at the expense of long-term air travel restrictions. Volatility on this stock is pretty high, so I recommend buyers of this company to fasten their seatbelt!